Travel hacking is a great way to save some serious money on travel. But it can get complicated fast, and risky if not done correctly. The good news is using points and miles to book travel isn’t an all-or-nothing game. You can just dip your toes in to start getting a feel of the benefits, or go all in to maximize free travel using credit cards. It’s 100% your choice how deep you want to go.

In this post, we will lay out each ‘level’ of travel hacking, from those who just want to accumulate a few points with no commitment, to those who are ready to jump in and fully maximize points and miles for travel. And we’ll give you some important rules, tips, and tricks to make sure you are successful at each level or your points and miles journey.

This post contains affiliate links. We may earn compensation when you click on the links at no additional cost to you.

Level 1: Sign up for Loyalty Programs

The easiest way to start accumulating a few points and miles is just to sign up for the loyalty programs for hotel chains and airline chains. After joining, you’ll earn points and miles based on miles traveled or dollars spent on flights and hotel stays.

Hotels

When looking at hotel loyalty programs, you’ll find that most hotels fall under one large loyalty program, like Marriott’s Bonvoy program, or Hilton’s Honor’s program.

There are a ton of hotel loyalty programs out there, from small with just a few boutique hotels, to huge with all types of hotels worldwide. And you can sign up for as many as you like for free! Becoming a member allows you to earn points for your stay, earn elite nights towards hotel status, and sometimes gives you access to ‘members only’ pricing and package deals.

Even though you aren’t limited in how many you can sign up for, you may want to book most of your travel through just one loyalty brand in order to maximize points and elite nights earned.

Here are the major hotel loyal programs for which you might consider when signing up.

- Marriott Bonvoy

- Hilton Honors

- World of Hyatt

- IHG One

- Choice Privileges

- Wyndham Rewards

- Best Western Rewards

- Radisson Rewards

Earning hotel points is pretty simple. Sign up for the loyalty program, then book hotels directly through the hotel’s website. You’ll earn points based on dollars spent- each program earns a different number of points per dollar spent.

In addition, for each stay, you’ll earn elite night credits, which count toward hotel status. So, using Marriott’s Bonvoy program as an example again, you’ll become a Silver Elite member after 10 nights per year. As a Silver Elite member, you’ll get free wifi, late checkout (if available), and you’ll earn 10% more points on hotel purchases. The more nights you stay, the better your benefits are.

Airlines

Unlike hotels, airlines don’t typically fall under a blanket brand. Instead, each airline will have their own frequent flyer program. However, many airlines are part of an alliance. The alliances will allow you earn miles on one frequent flyer program for miles flown on another airline within the same alliance.

There are three major airline alliances:

- Star Alliance (United Airlines is a member)

- Oneworld Alliance (Alaska Airlines and American airlines are members)

- Sky Team Alliance (Delta Airlines is a member).

For more details on these alliances, and who is a member, check out this helpful post.

Other airlines, like Southwest, JetBlue, and Hawaiian Airlines are not members of any alliance. However, they may still have partner programs that allow you to earn miles for spending on travel and more. For example, you can book hotels, car rentals, or even do some shopping through Southwest’s link to earn more miles on the Southwest Rapid Rewards program. Like hotels’ loyalty programs, they are free to join, so join as many as you like.

Who should do this?

Everyone! Loyalty programs are free to join and easy to use. Simply book travel directly through the website and earn points and miles.

For both hotels and airline loyalty programs, earning points and miles just through stays and flights likely won’t be enough to save a ton of travel. But you might get a free night or a free flight every once in a while. The only downside is you can’t use booking sites like Expedia. We actually prefer to book direct from the hotel or airline anyway because it reduces the chances of a mistake on the booking, and, if something goes wrong, it’s easier to fix when you are only dealing with one company instead of two (the booking company AND the airline or hotel).

Level 2: Get a co-branded card

Do you have a favorite airline or hotel chain? Or perhaps you have a favorite of both! A co-branded credit card can be a really easy way to start earning a lot more points and miles for one specific brand. Co-branded credit card just means that the financial institution, like Chase or American Express, has decided to work with a brand, such as Delta or Hyatt, to create a credit card.

Here’s how it works:

- Look for a co-branded credit card that meets your needs. Consider sign on bonus (will you be able to meet it), annual fee, best brands for you, and card benefits.

- Apply for a Co-Branded credit card, like the American Express Delta Gold Card, or the Chase World of Hyatt card.

- Start spending on that card. Be sure you don’t change your spending habits, and continue to only spend what you can afford.

- Track your spending to ensure you meet the minimum spend for the sign on bonus before the deadline.

- Pay your bill in full every month

- Watch the points add up

- Use your points to book travel

The great thing about co-branded credit cards is they make booking travel really easy. Your points will automatically show up on the loyalty website (for example, the it’ll be on your Delta Skymiles account), and you can easily search for availability and book. Also, you may get additional benefits, like free checked baggage or a hotel free night certificate.

You can switch all your spending to your credit card and rack up a ton of points that you would have never received just with your normal day-to-day spending. What a great extra bonus!

Who should do this?

Co-branded credit cards, like all credit cards, should only be used for those who can and will pay their balance in full every month. If you rack up a bunch of credit card debt and wind up paying interest, you’ll end up paying way more in interest than you are gaining in points.

Co-branded cards are great for those who are loyal to just one brand and who love the simplicity of the card.

For those that want more flexibility to book multiple airlines or hotel chains, a co-branded card might not be the one for you. Each co-branded card is different, but you’ll likely not get as high a value ($/point or mile) on your points and miles as you would with a good travel credit card that is not co-branded.

Level 3: Get a good travel credit card

Once you start using credit cards for points and miles, things can get complicated pretty fast. But for now, lets keep things fairly simple. Let’s assume you want one good card that allows you to book travel using a travel portal.

When you book travel through the travel portal, you’ll get a set value for your points. For example, if you get a Chase Sapphire Preferred card, you can book travel – flights, hotels, etc., on the Chase Ultimate Rewards portal for a set value of 1.25 cents/point. So if you have 80,000 Chase Ultimate Rewards points on your Chase Sapphire Preferred, you’ll always get $1000 in travel on the portal.

When booking through your credit card travel portal:

- Chase Ultimate Rewards points vary depending on the card: Chase Sapphire Preferred or Ink Business Preferred are worth 1.25 cent/point. Chase Sapphire Reserve are worth 1.5 cents/point. Most other Chase cards are worth 1 cent/point.

- American Express points are worth 0.7 cents/point

- Citi ThankYou points are worth 1 cent/point

- Capital One miles are worth 1 cent/mile

Booking through the portal is a great, simple way to book travel. But, if you want to get more money per point, you’ll need to look into transfer partners (see level 4 below)

There are a few things you may want to consider when choosing your card.

- Sign up Bonus and minimum spend to receive the sign on bonus. Make sure you will be able to make the minimum spend so you don’t miss out on the sign up bonus!

- Points valuation: Not all points and miles are equal.

- Annual fee. Annual fees vary greatly from $0 to $700+.

- Card benefits: Your credit card may have benefits like trip protection, rental car insurance, Priority Pass airport lounge access, hotel credits, etc. that may help offset the annual fee. The key is to make sure you consider which benefits you will actually use when deciding if the annual fee is worthwhile for you.

- Is the vacation you want bookable through the portal? Disney vacations are missing from many travel portals.

Who Should do this

We recommend this method for those who want flexibility and to save money on travel, but who prioritize simplicity.

For those who really want to maximize the value of their points, this may not be the best method for you. Your points are worth a lot less when booking through the portal than they’d be if you use transfer partners. It’s not uncommon to see double the value for points bookings done through transfer partners vs through the portal.

One other risk: booking through the portal means booking through a third party. So in the event of last minute cancellations (either by you or the travel company), natural disasters, sickness, whatever, booking through a third party adds a level of complication.

Level 4: Learn Transfer Partners

Booking free travel using points and miles is great. But, even better, is getting huge value for your points. While credit card travel portals offer you a set value for your points, transferring your points to partners can allow for a variable value, sometimes MUCH higher. But, if this is your first time hearing about transfer partners, you are likely already confused. So lets start at the beginning.

Credit card companies will allow you to transfer your points and miles to transfer partners. These are other travel companies with points and miles programs that have a relationship with your credit card company. Each transfer partner has different program rules and rates.

Transfer partners by credit card company. Note that not all transfer at 1:1. Confirm with your credit card the transfer ratio

Some transfer will use a set value of $/point just like your credit card company, but it might be higher or lower. Others will not have a set $/point value, and may have a points/mile traveled on an airline, or just points/night in high season or low season for hotels.

Ok, so the value of your points vary. But what is a good value for points? No simple answer there either, I’m afraid. But, for a good starting place, check out The Points Guy’s monthly points valuation. They update the valuation every month based on a ton of factors to give you an idea what your points can be worth.

So if you are booking travel, you can calculate the points value you’d be getting:

Cash rate/ points rate x 100 = cents/point

Chase Ultimate Rewards are typically valued around 2 cents per point. So if you were using Chase Ultimate Rewards, and you calculated a number lower than 2 cents per point, you may not be getting a great points value. If you calculate a number less than 1.25 cents, you’d want to book through the portal. And if you come up with a number over 2 cents, you are maximizing your points.

One important note: calculating your points value is really just for comparison purposes and bragging rights. Free travel is free travel and it really doesn’t matter what value you get out of your points as long as you are happy with it. But these rules of thumb give you a way to compare points bookings if that is something you care to do.

Hotel booking example

Lets talk through an example. Chase Sapphire Ultimate Rewards can be transferred to World of Hyatt, if you have a free World of Hyatt account (you do not need a credit card with them).

Transferring points: Before you transfer, make sure that Hyatt has availability to book on points for the hotel and dates you want. You won’t be able to transfer your points back to Chase after transferring. You’ll go to your Chase account, click through to the Ultimate Rewards site, and find the option to ‘Transfer Points’. You’ll see Hyatt listed, and you can click through to transfer.

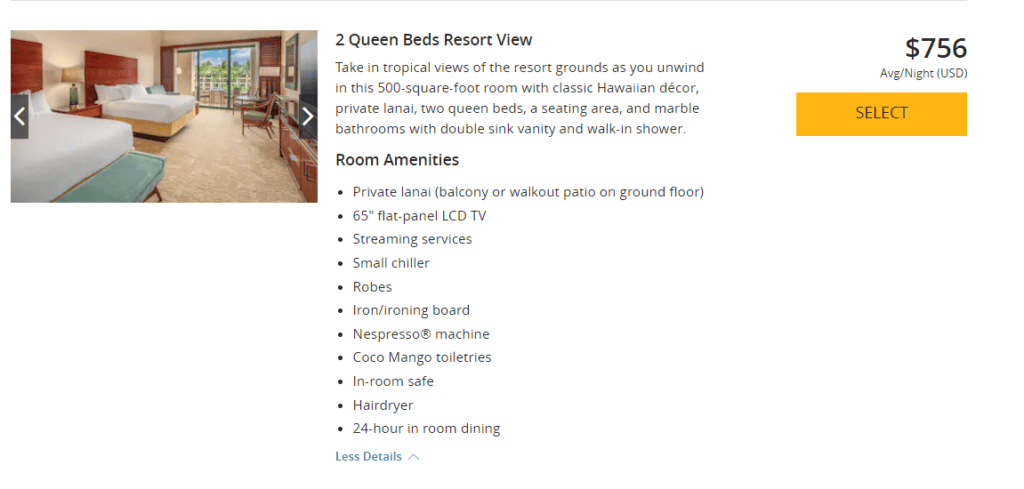

Book Travel: If you wanted to book a stay at the Grand Hyatt Kauai, and you find dates with availability. For the example, I’ve found dates available for 30,000 points/night.

For the same dates, you also have the option to book at a cash rate of $756/night. Note that this isn’t labeled as the EXACT same view- it appears Hyatt saves the ‘standard’ view for awards bookings only, but it’s the same room, and likely the same view.

For this stay, you’ll be getting a points valuation of $756/30,000 = 2.5 cents / point. So this is double the value you’d get when booking through the portal. I’d consider this a good value, and more than that, an opportunity to stay at a beautiful resort for free! I’d definitely book this room.

Once you login to your World of Hyatt Account, you should see the points you’ve transferred from Chase. Typically the transfer is instant but it could take up to 2 days. Booking on points is easy- just click through the ‘Book with Points’ option.

Simple Flight Booking example

Booking flights can get a bit more complicated. But lets start with the simplest way first. Just like with hotels, each credit card will have airline transfer partners. I want to book a one-way flight from Los Angeles to Honolulu.

First, I find I can book a direct flight on United Airlines from LAX to HNL for 15,900 United points and

The cash price for this flight is $208.50.

So if I do the math discussed above, I am getting ($208.50-$5.60) / 15,900 points = 1.28 cents/point. This is not great, but still a little better than the current value of 1.2 cents for United Points.

I am going to be transferring my Chase Ultimate Rewards Points, and I do have a Chase Sapphire. In the travel portal, I will be getting 1.25 cents/point. So if I chose to use points, this is going to be the lowest rate.

The process for transferring points is the same as the hotel example. You’ll go to your Chase account, click through to the Ultimate Rewards site, and find the option to ‘Transfer Points’. You’ll see United listed, and you can click through to transfer.

Who Should do this

Learning transfer partners is a great way to get a great value on points. But it does add a complex step when doing award bookings. This is great for anyone who is willing to take a little extra time learning transfer partners to save some extra money. We’d recommend it for most mid-tech savvy travelers.

Level 5: Booking with Airline Partners

Once you’ve figured out how to transfer points, you’ve MOSTLY got this travel hacking thing figured out. But there are a few nuances. Did you know that you can book a flight on one airline by using points from a different airline?

Airlines have Alliances and partners, as we discussed above. And each member of the alliance will release some award seats to its partners. This allows you to book seats on one airline through the awards program of another.

Sound confusing? Point.me is a subscription based tool that makes things MUCH easier. It’ll show you which flights are available to book on points, AND how to book it on partner airlines to make sure you are getting the best deal. It is current $12/month, but we think it’s well worth it for the value it provides.

Advanced Flight Booking Example

The best way to understand this method is with an example, so let’s jump into it.

Delta and Virgin are both members of the SkyTeam Alliance. Delta often charges a lot of points for a booking. So, as an alternative, you may be able to book a seat on a Delta flight through the Virgin Flying Club program. Virgin’s rewards program is based on miles flown, and starts at just 7,500 points for up to 500 miles, so there are lots of great deals to be found. The bad news is that availability is limited- sometimes very limited. But it is a great option.

Here is an example flight. I want to go from Atlanta, Georgia to London. I am just showing a one-way flight just to keep things simple. If I book this flight through Delta on their SkyMiles program, it’ll cost me 96,000 SkyMiles. Whoa! I don’t have those points. And Delta’s only real transfer partner is American Express- not a lot of options here. Lets try again.

If I book the exact same flight through the Virgin Flying Club Program, it’ll only cost me 22,500 miles. MUCH better.

And, more importantly, Virgin miles are easier to get. You can transfer Chase Ultimate Rewards, American Express Membership Rewards, Citi ThankYou Points, CapitalOne Miles and Marriott Bonvoy points to Virgin Flying Club.

For the example, lets use Citi ThankYou Points. First, you’ll create a Virgin Flying Club account, if you don’t already have one. Note that if you are creating the account, you’ll have to wait 24 hours before you’ll be able to make the booking.

Once the account is created, log into your Citi account, and click on your points balance to take you to the ThankYou site. Under the Travel tab, you’ll find the option to transfer points, and you’ll be guided through the transfer of points to Virgin. Once your Virgin account is more than 24 hours old, the transfer should be instant, but it can take up to 24 hours.

Booking is easy through your Virgin Account. Just log in, and go through the booking, making sure you chose to show price in points.

Who Should do this

Booking through partner airlines takes a bit of finagling, and a lot of patience. It is a great way to find some serious deals, especially for business class flights. But there can also be a lot of frustration, learning how to book on each partner airline, having very limited availability on partner airlines, etc.

People who are fairly tech savvy, and who enjoy the challenge of finding a great reward seat are best suited to booking through partners. If this already feels too complicated, and you aren’t interested in learning, then don’t! There are great deals to be found without going this route.

Level 6: Sign up for new credit cards and Earn Bonuses

Ok, now that you know all the best ways to book flights and hotels and get a great redemption, how are you going to get a LOT more points? Sign up bonuses. A lot of people get nervous pretty quickly when we start talking about opening new cards, but don’t panic just yet. Believe it or not, you can maintain a very high credit score and not accumulate debt if you follow some basic rules.

- This is the most important: make sure you can pay off your credit card in full every month. Don’t increase your spending when you open a new card. Just put your normal expenses on a credit card rather than a debit card.

- Rule of thumb: only open a new credit card every 90 days. This is a rule that can be broken, but it’s a good place to start.

- Understand your eligibility for a sign up bonus

- Have a plan for how to meet the minimum spend so that you’ll always get the sign up bonus

- Wait at least one year before cancelling. Then consider cancelling or downgrading the card if the annual fee isn’t worth the benefits for you.

- Make sure you get a good sign up bonus. Credit cards change the sign up bonus all the time, so you’ll want to keep an eye out for the higher bonuses, and apply then. We love Travel Freely because they always show you the best offer currently available, and tell you how it compares to the ‘standard’ offer.

If you follow these rules, you will stay in good standing with your banks, and maintain a good, or great, credit score, and be able to rake in those credit card points for lots of free travel!

So lets get into a few of the details before you begin

5/24 Status

5/24 is a rule that is specific to Chase. But tons and tons of great travel credit cards are Chase cards, so it ends up being a pretty important rule. Chase will not approve you for a new credit card if you have opened more than 5 new personal credit cards in the last 24 months. That includes all new cards you’ve opened from any bank (not just Chase account), plus any accounts for which you have been added as an authorized user.

If you are over 5/24, you can still open cards from other banks. Just know that it’ll push even farther over the 5/24 limit, which means you’ll have to wait even longer to get a new Chase card.

American Express Lifetime Rule

American Express does things a little bit differently. They don’t have as strict a rule on how many cards you can open a year. However, they do have a limit on how many times you can get a sign on bonus, and that is only ONCE per card, forever. So if you have opened an American Express Gold ever before in your life, and received a sign up bonus, don’t bother applying again because, even if they give you the card again, they will not give you a bonus.

Canceling a card

Want to cancel your new credit card after getting the sign up bonus? There are a couple things to consider there as well.

There is often a statement in the fine print of your credit card contract that says if you cancel before 12 months, they can take back your bonus points. You may be contractually obligated to pay the annual fee as well, regardless of if you’ve canceled your card. So you may as well keep it and take advantage of the benefits of the card for the first 12 months.

After your 12 months is up, you are free to cancel. But beware that closing an account can impact your credit score. There are a few options. You can try getting in touch with your credit card company to ask if there is a retention offer. They may credit your account for the annual fee, or offer you bonus miles to sweeten the deal and make it worth while for you to keep the card another year.

If there is no retention offer, or you don’t like the one they’ve made you, you can also consider downgrading the card to a no annual fee card. That way, you’ll have no impact on your credit score, but you won’t have to worry about paying the annual fee every year.

Referrals

Once your spouse, friends, or family start to see how many points you can get by opening a new credit card, they might want to get in on it too! The great news is you can send them a referral link. That way they can still get a get great sign up bonuses (SUB), AND it’ll give you some serious bonus points as well (often 20,000 bonus points).

One method lots of families like to use is that one spouse, lets call her Player 1, will open a new credit card. As an example, lets assume that the SUB is 80,000 points after spending $4,000 in the first 3 months. The referral bonus is 20,000 points, with a limit of 5 referral bonuses per year. Once Player 1 meets the minimum spend, she’ll refer her spouse, Player 2. Player 2 will apply with the referral link and start spending towards the minimum spend. In the end, Player 1 and Player 2 will get a total of 180,000 points for their two cards- great deal and a good chunk of points!

Who Should do this

If you decide to open credit cards to get those extra credit card points, be sure you can meet the minimum spend to always get that sign up bonus, and, most importantly, that you can always pay your balance in full, every month. If you retain a large credit card balance, you’ll end up paying more in interest than you are earning in points.

Level 6: Sign up for Business credit cards and earn bonuses

Once you start raking in those points and miles, it’s hard to stop. And soon that 5/24 rule starts to feel more and more limiting. So what is the workaround? Business cards. Business cards do not count towards your 5/24 status, which allows you to open more than 5 cards every 2 years. However, you do have to be under the 5/24 rule to qualify for Chase credit cards. If you are over 5/24, you can still get a business credit card from another bank, and it will not impact your 5/24 score like a personal card would. Plus, business cards give you so many more options for great cards with great sign up bonuses.

Do I even qualify?

Business cards are easier to qualify for than you might expect. You don’t have to be a full-time business owner with a huge income. You can have a rental, be a gig worker, independent contractor, have an Etsy shop, or even just sell things on Facebook Marketplace and potentially get approved.

With the exception of the 5/24 rule, business credit cards are going to be similar to personal cards, and you should follow the same rules. One note: often, the business card issuer will include a statement in your agreement that the card can only be used for business purposes. While it’s virtually impossible for the card issuer to be able to tell if your purchase is business related or not, it’s something you’ll want to keep in mind if you decide to jump into the business card game.

Who Should do this

This method is great for those who qualify for business credit cards, and those who can spend on a credit card without overspending, and pay their balance in full every month. Also, you’ll want to really think about the minimum spend requirements – some business cards have a hefty minimum spend in order to earn the sign up bonus. It’s only worth signing up if you will spend the minimum in the allotted time.

Level 7: Maximize points earned by using the right card

Maximizing categories takes a little extra effort, and requires some organization. But you don’t have to have be opening a ton of new cards all the time to participate. In fact, anyone who has a couple of credit cards can start maximizing spending for the cards you have.

Here’s how it works: Each credit card has slightly different structures for issuing points. For example:

- Chase Sapphire Preferred gives 3X points on dining and streaming services, with most other categories at just 1x points

- American Express gold offers 4X on groceries and dining and 3x on flights

- Chase Freedom Flex offers 5X on one category, which changes each quarter, 3x on dining and drugstores, and 1x on most everything else

These are just a few examples. There are hundreds of cards that are going to pay out points using different structures. The key is to understand which card you should be using for which category. That way, you are ALWAYS getting 3, 4, 5X points instead of just the 1X that you’d typically get.

For example, if you have all three of the cards listed above (Chase Sapphire Preferred, American Express Gold, and Chase Freedom Flex), which one will you use to pay for groceries? Because both American Express Membership Rewards and Chase Ultimate Rewards are currently valued at 2 cents/point, and AmEx Gold offers 4X rather than 3X, you’d pick the AmEx. But what if the Chase Freedom Flex’s 5X rotating category is current groceries? Than you gotta go for the Chase Freedom Flex!

You can see how this can become complicated very quickly. But the payout of maximizing categories can be huge. If you are spending $1,000/month on every day purchases, and you can maximize your spending to move from 1x to 5x, you’ll go from earning a measly 12,000 points/year to a substantial 60,000 points/year.

And of course, there is help out there. Check out the Card Pointers app. You simply put in which credit cards you have (no need to enter any account information, just the cards name), and the app will help you figure out which card is right for which spending category.

We’ve also seen people just put a post-it note on each card explaining the main categories just as a reminder. Whatever works for your to make sure you maximize that spending and get the most points possible!

Who Should do this

People who are organized and motivated to maximize their points should use this method. It also works best if you have at least a few credit cards to chose from, or be open to opening new credit cards that maximize the categories where you spend most of your money.